Chart(s) of the Day: February 17, 2023

A fundamental reason for a bearish bias.

Housekeeping note: I apologize for missing a couple days of charts. The kiddo has had a rough couple of days due to typical daycare sickness. Hopefully we’ll be back on track by Monday.

Today’s charts provide some long-term hope for the bears.

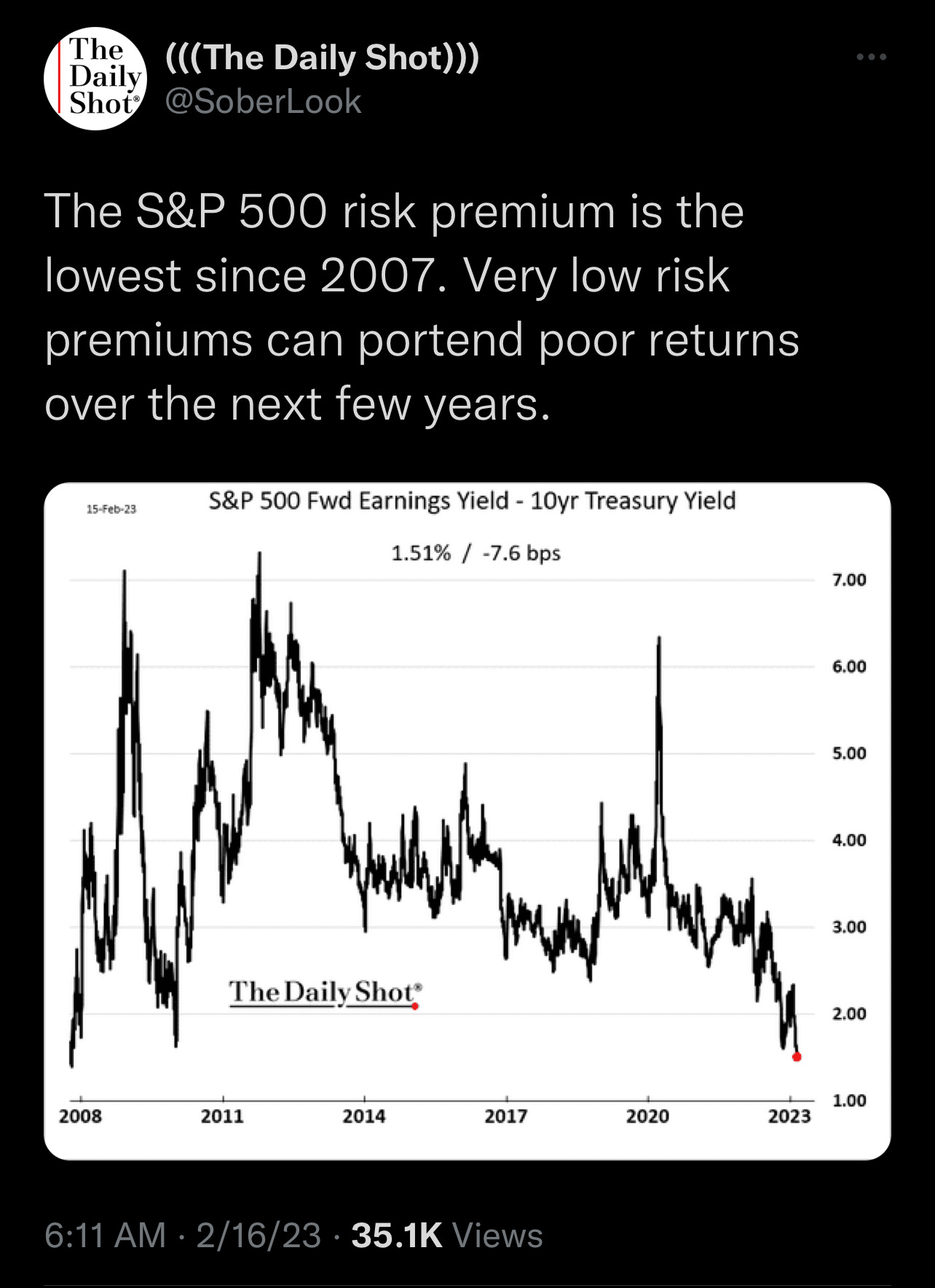

Figure 1 comes from @SoberLook, publisher of The Daily Shot newsletter.

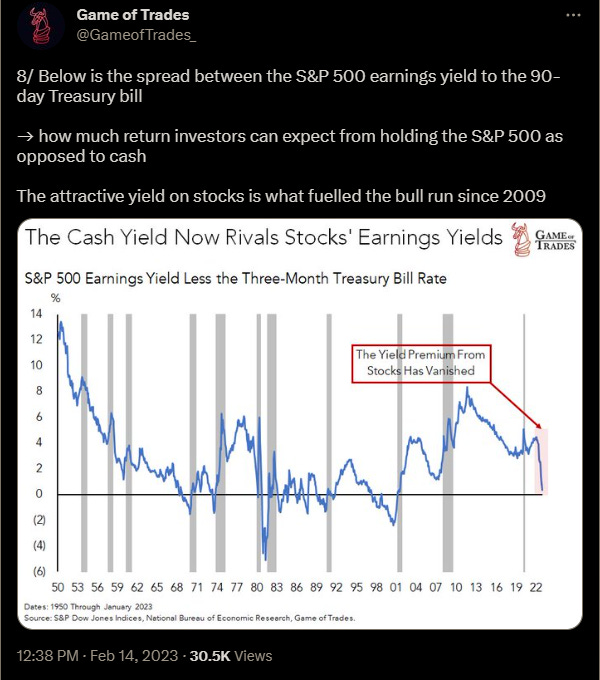

Figure 2 was published by @GameofTrades_

Both of these charts use different calculations, to measure the same metric — the current risk premium on the S&P 500. A risk premium tells you how much compensation is being paid for taking risk. In this case, how much an investor is to earn investing in the S&P 500 above and beyond what they can earn without taking any risk.

Figure 1 shows the S&P 500 risk premium dropping to levels seen prior to the 2008 financial crisis. The S&P 500 was a poor investment in the subsequent 4 year period between 2007-2011, especially when compared to the return earned on government bonds. Figure 1 suggest investors are not currently being compensated for the risk they are taking investing in the S&P 500 — as the spread is only 1.5% between the S&P 500 earnings yield (inverse of the P/E Ratio) and the 10 year US treasury yield.

Figure 2 shows a similar calculation to Figure 1, although it uses the yield on 3 month treasury bills instead of the 10 year treasury bond. Compared to the 3 month T-bill, investors in the S&P 500 have not been paid so little for taking equity risk since near the peak of the Dot Com bubble in the late-1990s. Investor’s are being compensated less for risk today then at the peak of the housing bubble in 2007. This is suggestive of low expected returns from equity investments moving forward.

Long-term equity investments are best made when the risk premium on stocks is high, such as in 2020, 2009, 2003, 1994, 1974, etc.

Risk premium’s usually spike higher during recessions and market panics, providing investors that are willing to take risk and invest when it feels uncomfortable the opportunity to earn significant future returns.

— Brant

Disclaimer: The content provided on the Capital Notes newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision. Always perform your own due diligence.