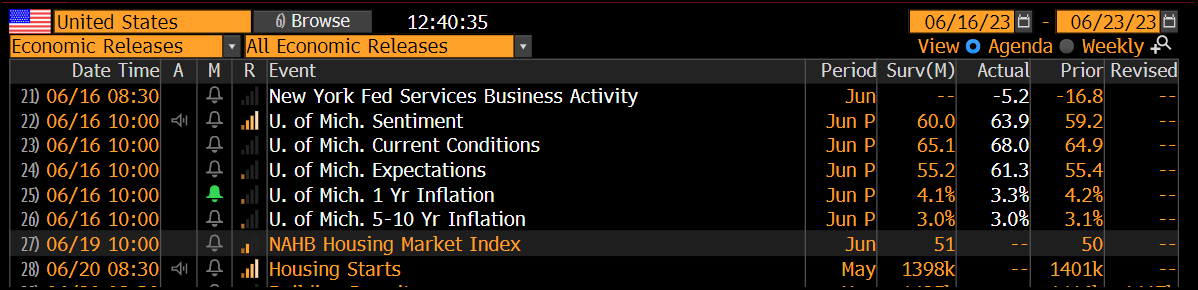

We received more data about an hour ago that inflation continues to decline back to normal levels. The chart below is data from the University of Michigan Consumer Sentiment Survey. This shows the survey's estimate of 1 year ahead inflation expectations came in far below expectations, 3.3% Actual vs 4.1% Expectations.

This data helps to confirm some of the leading indicators of inflation we've been highlighting over the last several weeks, such as the Fed Global Supply Chain Index that leads inflation by 6 months. Here is what we said 3 weeks ago about this relationship:

Chart of the Day: May 22, 2023

My base case is for inflation to continue to decline as Owners Equivalent Rent (OER) finally begins to reflect more recent rental market data and work its way into the CPI data.

In my opinion, the risk to falling inflation --- this is NOT my highest probability case, but one that is increasing in probability after recent market action --- is agricultural and energy commodity prices. We've recently seen a resurgence in ag commodities as dollar weakness has accelerated, see ticker symbol DBA. Also, natural gas, oil, and their derivatives, such as gasoline, look ripe for a move higher in at least the near term. Remember, we are still draining the Strategic Petroleum Reserve (SPR). When the Department of Energy decides to refill the SPR it could create significant upward pressure on oil prices.

— Brant

Disclaimer: The content provided on the Capital Notes newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision. Always perform your own due diligence.