What's happening in the housing market?

Is recent price weakness the start of a larger contraction?

Housing is a constant topic of discussion in the finance and economics world as it drives much of the wealth effect that influences credit creation, spending, and economic growth.

Since the 2012 lows, home prices in the US have been on a seemingly endless march higher [Figure 1]. Housing cycles last a long time — it’s the nature of the market. Due to this, every cycle produces a group of investors that believe “this time is different” — that housing is a zero risk investment that will never fail. That home prices “only go up”. This group always seems correct, for awhile.

Figure 1 shows that home prices peaked in mid-2022 and have experienced 7 consecutive months of declines for the first time since the 2006-2012 home price bear market. Is this likely to continue, or is this simply another buying opportunity?

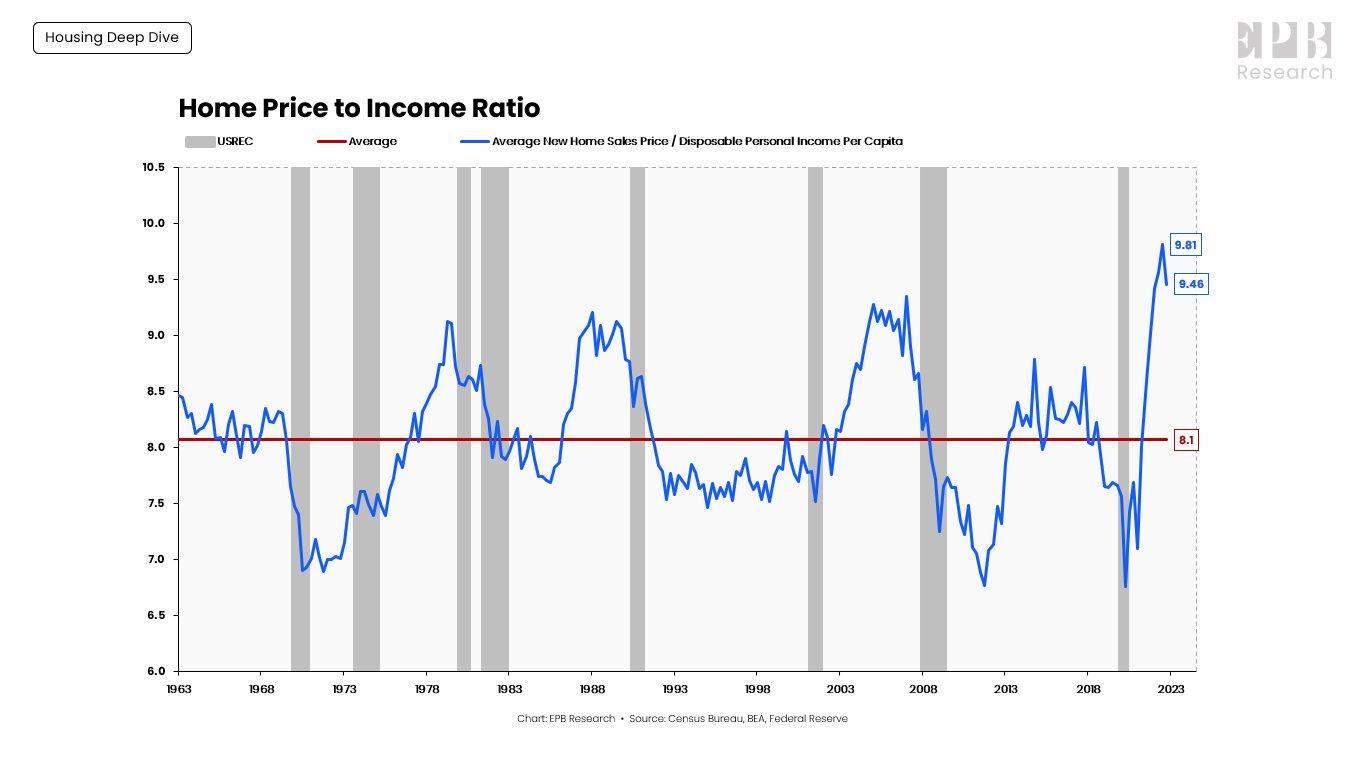

Figure 2 and Figure 3 do a much better job showing the extent of today’s home price “overvaluation”.

The average US home is now selling for 10x the average US income. Going back to 1963, this is a historic high. In fact, even after the last 7 months of price declines, the home price to income ratio is still higher than the peak of the housing bubble in 2007.

As mentioned in Figure 2 by EPB Research (who I highly recommend following), extreme home price overvaluations can persists for 2-3 years before they begin to unwind.

Figure 3 is simply a close up of the chart produced by EPB Research in Figure 2, for anyone that wants to zoom in for a closer look.

Other than historic overvaluation, what could speed up the home price revaluation? One of the reasons why home prices can remain overvalued for long periods of time is due to the ease with which lenders will provide credit when real estate is used as collateral. Higher home prices can create a reflexive, positive feedback loop where banks are more willing to rely on real estate as collateral, therefore they are willing to raise their LTV limits, leading to more credit, higher home prices, lower LTV limits, and so forth.

One catalyst that has often led to the end of a housing bull market is banks finally deciding to begin raising lending standards — thus stopping the positive feedback loop and potentially even sending it in the other direction.

Figure 4 shows lending standards are now tightening rapidly for the first time since the lockdown phase of the pandemic. This also happens to be the first time banks have been tightening lending standards into the face of a overvalued housing market since 2007.

Is there anything else that can contribute to an acceleration of the house price downtrend?

How about supply? When I hear people discuss the housing market, they always point out the lack of supply as a reason why home prices have to rise higher and higher as if they were a perpetual motion machine. Maybe supply was limited over the last decade, as the market tried to adjust to the low levels of construction during the depths of the housing crisis from 2009-2013 — but Figure 5 shows this may no longer be the case.

Figure 5 shows there are now near the same amount of new home inventory on the way as there was at the peak of the bubble in 2006-2007. The massive increase in prices post-pandemic finally jump started a supply response from the home construction industry.

So, is recent weakness the start of a larger contraction in home values? Maybe.

We have:

historically high price to income ratios

tightening lending standards

a coming wave of new home inventory

Historically, this has been a lethal combination for housing bull markets. But as I mentioned at the beginning of this post, housing markets can stay irrational and overvalued for years before they finally contract back into an affordable range.

Time will tell.

— Brant

Disclaimer: The content provided on the Capital Notes newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision. Always perform your own due diligence.