Chart(s) of the Day: February 28, 2023

Are markets correctly pricing a deterioration in credit conditions?

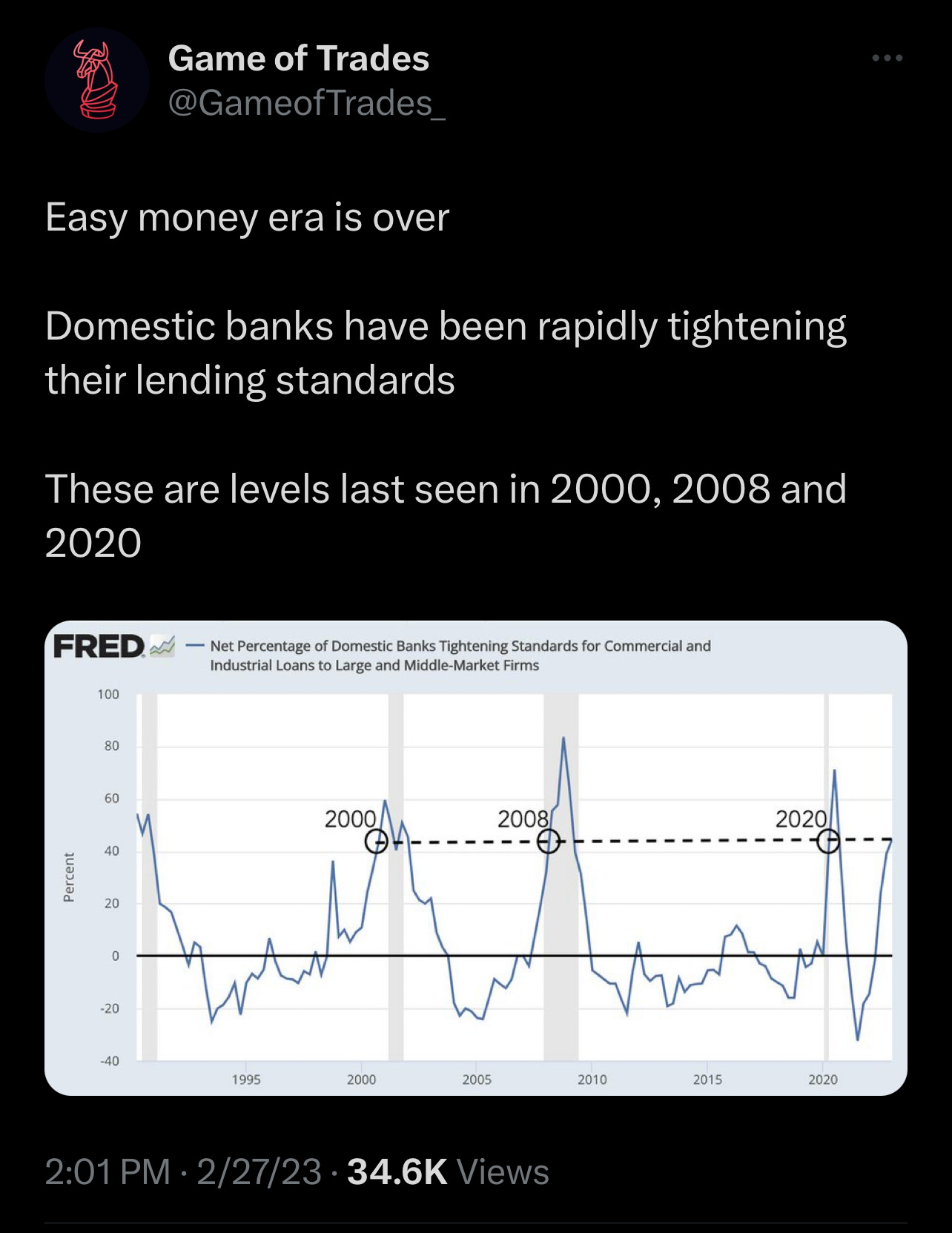

Today’s Chart(s) of the Day takes a look at bank lending standards and their relationship to recessions and high yield bond spreads.

Both Figure 1 and Figure 2 display the results of the Senior Loan Officer Opinion Survey on Bank Lending Practices. Here is a description from the Federal Reserve:

“The survey, conducted by the Board of Governors, is currently sent to 124 domestic banks and US branches and agencies of foreign banks. The senior loan officers at those organizations answer a series of questions about their opinions on current lending practices. This qualitative information is used by monetary policymakers to gauge credit market and banking conditions.”

Figure 1 shows the fraction of domestic banks that reported having tightened their lending standards minus the faction of banks that reported having eased their lending standards on commercial loans to large and middle-market firms. In other words, as the blue line in Figure 1 increases it represents more stringent lending standards.

It’s important to review a basic economic feedback loop — what we call a reflexive feedback loop — in order to form a conclusion based on Figure 1. Lending & spending positive feedback loop:

One person’s spending is another person’s income1

Most US dollar money creation occurs through the process of bank lending

Borrowing allows one to increase their spending above their level of income

Banks make loans to meet the spending needs of their qualified customers

When banks reduce lending standards, more customers qualify for loans, lending increases and spending increases

When spending increases, incomes increase

When incomes increase, more people become qualified bank customers

As more people qualify for loans, lending increases further, incomes increase further… etc…

Also, as lending and spending increase through this process, it will lead to an increase in asset prices — as assets rise in value, they can be used as collateral to support an additional increase in borrowing and spending, increasing incomes and asset prices even further, leading to more borrowing, etc…

This is a positive feedback loop that begins with the reduction of lending standards and is driven forward as lending increases, spending increases, and as a result incomes increase — which leads to a further increase in lending.

It is important to understand that this entire feedback loop also works in reverse. When banks tighten lending standards significantly it will result in a reduction in borrowing as fewer customers qualify. When borrowing falls, spending drops, incomes decline, and asset prices head south — this leads to even less borrowing, an additional drop in incomes, even lower asset prices, etc.

Now that you understand these basic economic feedback loops, take another look at Figure 1. It’s no coincidence that every time the net % of banks tightening lending standards reaches 40%+ a recession soon follows. We’re now at that level in the current cycle.

What does all of this mean for risk assets? Figure 2 shows the same survey results as Figure 1 (red and blue lines). However, it also shows the ICE BofA US High Yield Index Option-Adjusted Spread (green line). This index measures the spread between the yield on high yield corporate bonds and US treasury bonds. When the green line rises, the financial markets are pricing in a high degree of credit risk and an increasing probability of bankruptcies. This is usually accompanied by significant declines in the value of risk assets like stocks, industrial commodities, cryptocurrencies, etc.

Historically, there is a high correlation between the net % of banks tightening lending standards and high yield spreads (Figure 2), which makes intuitive sense. If banks are tightening lending standards, it’s because they believe an environment exist where the probability of bankruptcies and high credit losses is increasing. A rapid rise in high yield spreads is the bond market’s way of confirming the bank’s rationale for tightening lending standards.

In Figure 2 there is a clear divergence between the red/blue and green lines. High yield spreads are not confirming the rapid increase in bank lending standards. To make it clear — the financial markets are not yet pricing in the increased probability of credit losses and bankruptcies that banks see on the horizon. This can mean one of two things:

The analysis driving banks to tighten lending standards is wrong.

Financial markets are behind the curve and late to the game pricing in the risk of increased credit losses.

If #1 is correct and high yield spreads are reflecting the true state of the credit markets, banks will realize this soon, begin easing lending standards and economic growth will accelerate.

If #2 is correct, a recession is likely in the cards for sometime in the 2nd half of 2023 and the financial markets have not yet priced it in. Which could result in a rapid re-pricing of risk assets to the downside.

What way will it go?

— Brant

Disclaimer: The content provided on the Capital Notes newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision. Always perform your own due diligence.

When referencing “person” here a person could be any entity. It could be an individual, a business, a government, etc.