Rate Cuts Increasingly Unlikely

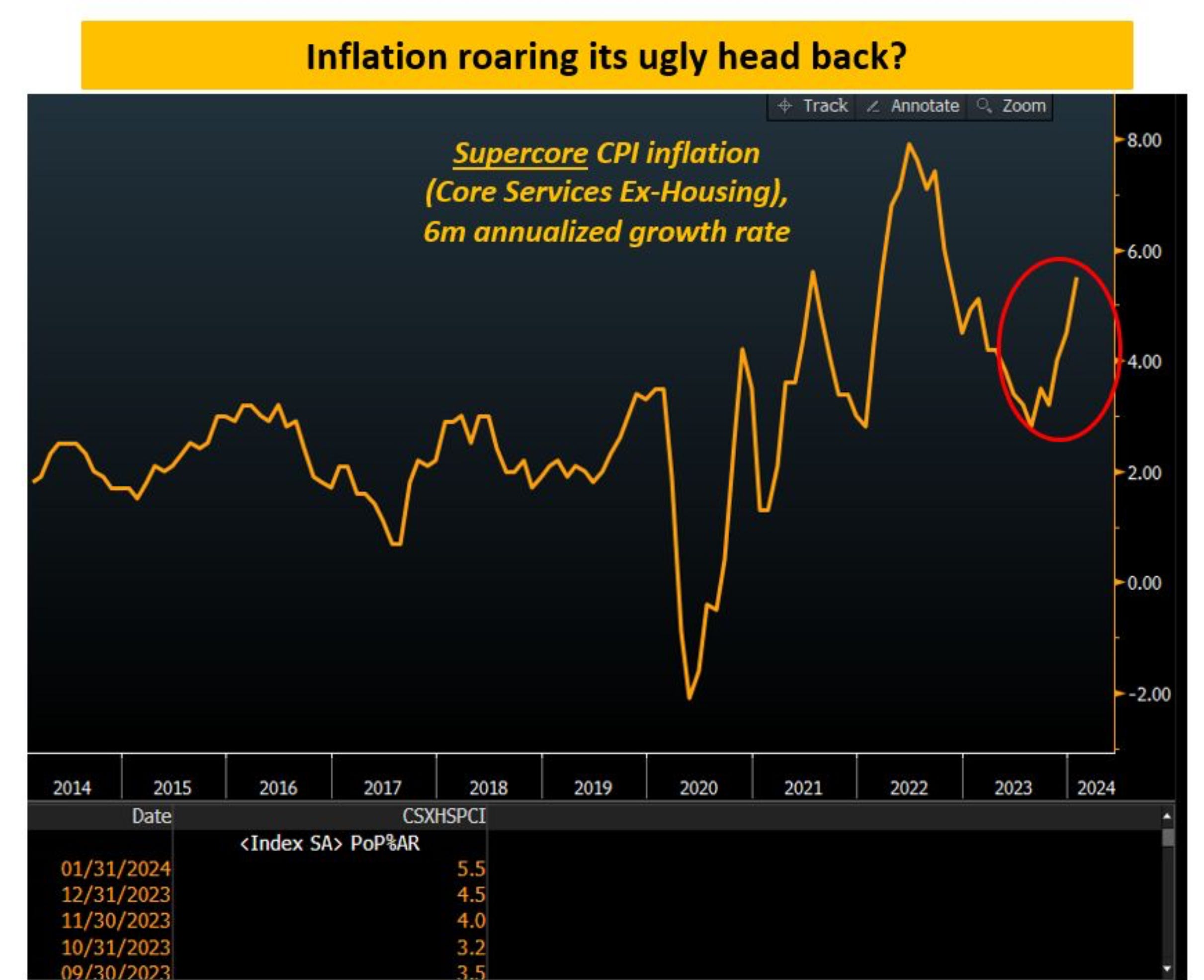

Supercore inflation accelerates higher.

One of the reasons I began to turn cautious on the rally back in early-January was sentiment starting to reach positive extremes that are typically associated with low returns over the intermediate term. I discussed this in my post on January 2nd. You can find it here: “Is Santa Exhausted?”

Another reason was the market getting ahead of itself in the pricing of future Federal Reserve rate cuts. At the time, the market was pricing in 6 to 7 quarter point rate cuts, for a drop in the Fed Funds rate during 2024 of 1.5%+. At its most dovish, markets had priced in a near certainty of Fed cuts beginning in March.

These expectations seemed unlikely to me with inflation becoming quite sticky around 3% and the likelihood of Jerome Powell to continue cautiously protecting his reputation (an attempt to prevent another “transitory” narrative fiasco).

My expectation was the move from 3% annualized CPI growth to 2% would prove to be much more difficult than the market seemed to believe.

Today we have received more data pointing this out. In other words, inflation continues to prove sticky, especially in the core services area that the Fed cares so much about.

Check out the chart below from Macro Alf.

As Macro Alf says in the post linked to above:

“Well - as the chart shows, supercore inflation has re-accelerated from 3% late last year to 5.5% (!) on a 6-month annualized basis.

As a result, bond markets are busy pushing Fed cuts further in the 2024 calendar.

My screen says no chance in March, and only a 50% chance of a cutting cycle starting in May.”

I imagine even the 50% chance of a May rate cut is still far too dovish and we will see it coming down in the coming weeks.

Could this be the catalyst needed to kick off a correction in equities and other risk assets?

Maybe. Timing the exact top of a uptrend or the exact bottom of a downtrend is something that no one should ever claim capable of doing consistently. I’m still net long myself. But sentiment and positioning remains overbullish1 and the short term price uptrend is at risk of breaking. This calls for more attention to be spent on risk management vs the deployment of capital into new long positions.

A solid break of the short term uptrend, one that started in October 2023, would likely target a return to the 4600-4700 area on the S&P 500. This potential 6%-9% correction would likely be enough to reset sentiment and lower valuations enough to provide investors with a decent buying opportunity.

— Brant

Below is a quick sentiment and positioning check using data collected, in order of appearance below, from Macro Ops, Markets & Mayhem, Raoul Pal, and the CNN Fear & Greed Index.

Disclaimer: The content provided on the Capital Notes newsletter is for general information purposes only. No information, materials, services, and other content provided in this post constitute solicitation, recommendation, endorsement or any financial, investment, or other advice. Seek independent professional consultation in the form of legal, financial, and fiscal advice before making any investment decision. Always perform your own due diligence.